WATERS CORP /DE/ (WAT)·Q4 2025 Earnings Summary

Waters Beats Q4, Completes $4B BD Deal to Create $6.4B Life Sciences Giant

February 9, 2026 · by Fintool AI Agent

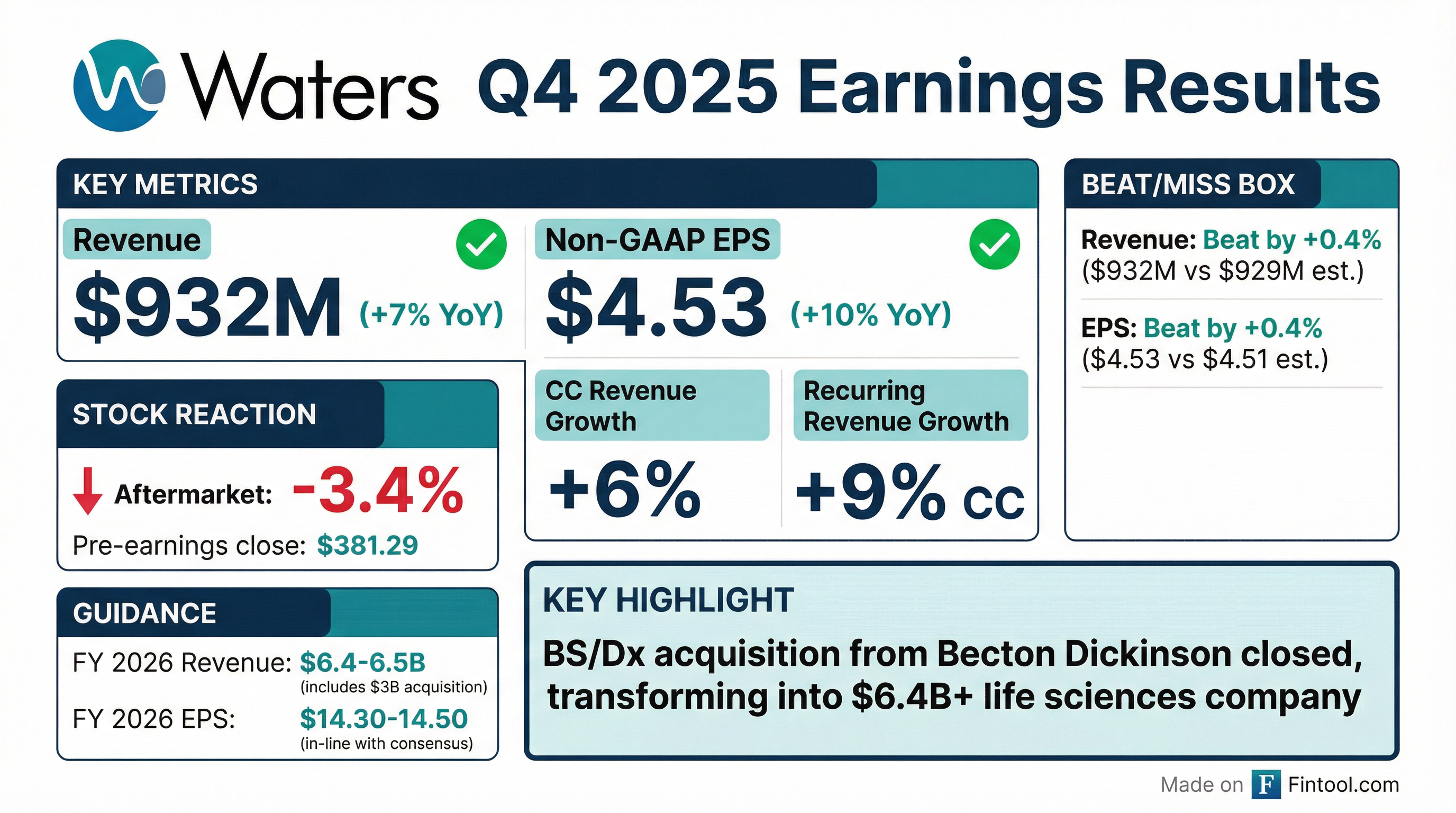

Waters Corporation delivered a solid Q4 2025, beating estimates on both revenue and EPS while closing its transformational acquisition of Becton Dickinson's Biosciences and Diagnostic Solutions (BS/Dx) business. Revenue grew 7% to $932M with non-GAAP EPS of $4.53 (+10% YoY), driven by 9% recurring revenue growth and strength in pharmaceutical end markets.

Despite the beat, the stock fell ~3.4% in after-hours trading as investors digest the integration risks of the $4B acquisition and diluted near-term EPS from acquisition accounting.

Did Waters Beat Earnings?

Yes — modest beat on both lines:

Full-year FY 2025 results were equally solid:

Waters has now beaten estimates for 8 consecutive quarters, demonstrating consistent execution through the life sciences funding downturn.

What Drove the Beat?

The outperformance was powered by three key factors:

1. Recurring Revenue Strength (+9% CC)

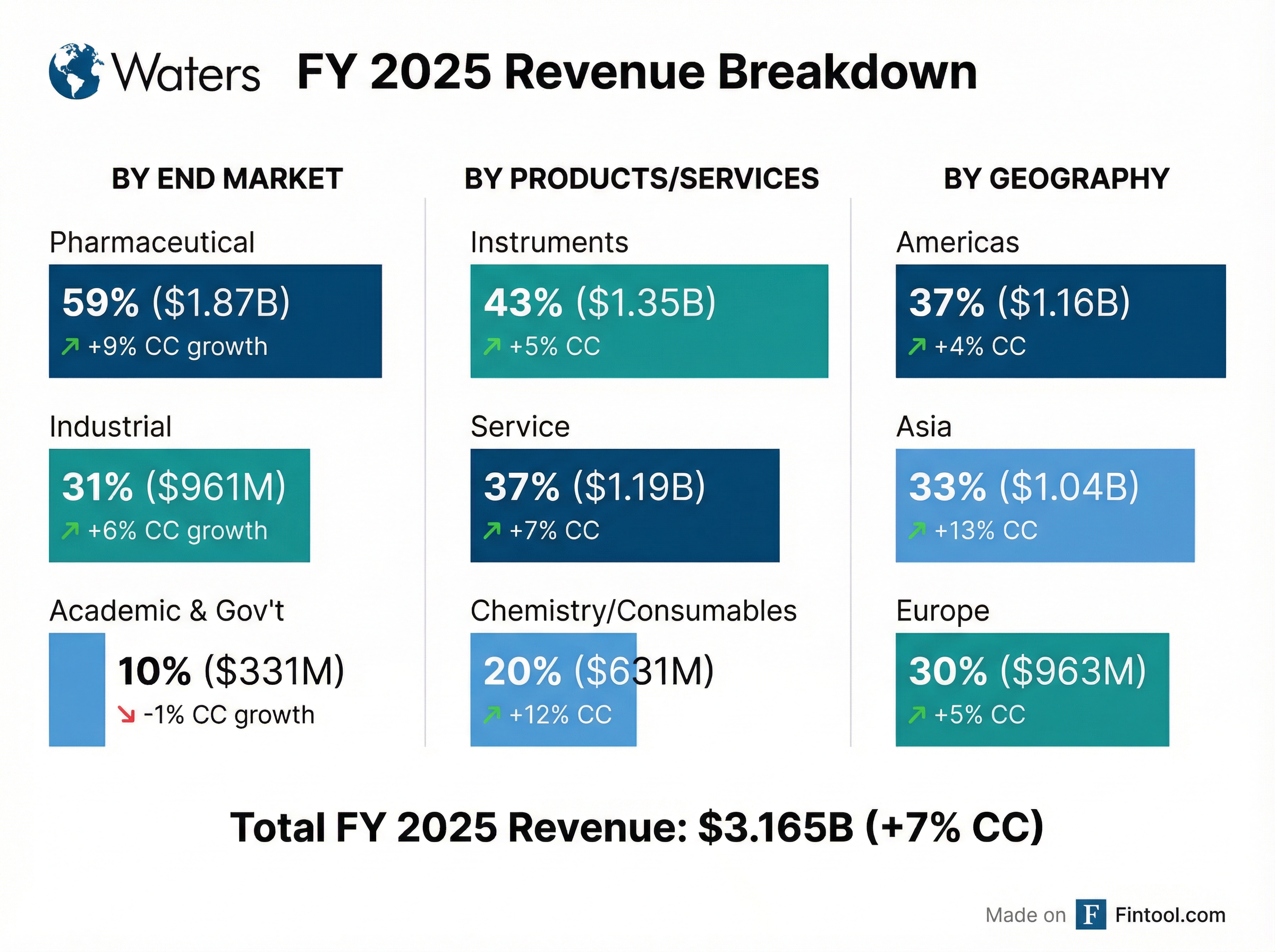

Service revenue grew 8% and chemistry consumables surged 12% in constant currency, reflecting strong instrument utilization and consumables pull-through. Service plan attachment reached 54% of the active installed base (up from 50% in 2024).

2. Pharmaceutical End Market Momentum (+9% CC for FY)

Pharma, representing 59% of revenue, grew 9% for the full year with strength across all geographies. Asia ex-China was particularly strong at +16%.

3. Idiosyncratic Growth Drivers

Management highlighted three specific tailwinds:

New product launches also outperformed, with Alliance iS sales growing 2.1x, Xevo TQ Absolute +33%, and MaxPeak chemistry +36% in constant currency.

What Did Management Guide?

Waters provided its first guidance as a combined company following the BD acquisition:

FY 2026 Guidance

Q1 2026 Guidance

The organic business guidance of +5.5-7.0% CC growth is at the upper end of life sciences tools peers, reflecting Waters' idiosyncratic growth drivers and commercial execution.

What Changed From Last Quarter?

The biggest change is the company itself. With the BS/Dx acquisition now closed, Waters transforms from a ~$3.2B analytical instruments company into a ~$6.4B life sciences platform spanning:

New Four-Division Structure

Waters has reorganized into four divisions, each following its repeatable business model:

Acquisition Execution Playbook

Management outlined their plan to apply Waters' commercial execution playbook to the acquired business:

2026 Synergy Targets: $55M cost synergies + $25M EBIT from $50M revenue synergies = $80M total EBIT contribution.

How Did the Stock React?

Despite beating estimates, WAT fell ~3.4% in after-hours trading:

The negative reaction likely reflects:

- Integration complexity — The BS/Dx deal adds significant operational complexity

- Near-term EPS dilution — GAAP EPS guided at $6.63-6.83 vs non-GAAP $14.30-14.50 due to $5.24 of purchased intangibles amortization

- Debt overhang — The acquisition was largely debt-financed, with FY 2026 net interest expense of $179M

The stock has rallied ~27% since late September 2025 ahead of the acquisition close, so some profit-taking was expected.

Key Metrics to Watch

Commercial Execution KPIs (Standalone Waters)

Idiosyncratic Growth Drivers (2026-2030)

Management expects 5 idiosyncratic drivers to contribute 200+ bps of annual growth accretion:

- GLP-1s — Triple-specced position across orals and injectables

- PFAS — Expanding into food & materials testing

- India Generics — Volume growth from patent cliff and aging population

- Biologics — New bioseparations launches, FDA biosimilars opportunity

- Informatics — Empower subscription transition

Q&A Highlights

On BD Business Performance and 2026 Outlook

Analyst Tycho Peterson (Jefferies) pressed management on the deteriorating BD results versus the original deal model. CEO Udit Batra acknowledged:

"Several issues emerged in Q4 that impacted the growth of both of those businesses that were not fully known in Q3... This reminds me of Waters almost five years ago."

CFO Amol Chaubal detailed the Q4 headwinds:

- China DRG: Increased focus on reducing consumption in diagnostics testing

- Government shutdown: Export approvals to China were delayed

- Weaker flu season: Impacted point-of-care business vs. prior year

Importantly, management emphasized these headwinds are now in the baseline for Q1 guidance of a low single-digit decline, with recovery expected through the year as DRG comparisons ease in Q3/Q4.

On Pricing Discipline (Deal Desk)

Management outlined plans to implement Waters' pricing discipline at BD:

"The first is a centralized examination of what the list prices are, as well as what the discounting is. That escalates all the way up to me as discounting requests come from the different regions. Basically, we take away the ability for regions and sales teams to discount."

Batra noted BD's reagents — dyes and antibodies — are "highly differentiated products that only BD produces" with "zero reason why there should be discounting there."

For context, Waters' chemistry business achieves 400-450 bps stick rate on like-for-like list price increases, vs. BD's historical 40-50 bps.

On Empower Subscription Transition

A key topic was the transition of Empower informatics from on-prem licenses to subscription. Batra confirmed:

"Two of the top five pharmas converted. Q1 funnel is strong."

The transition creates a low single-digit headwind to instruments in Q4 as revenue shifts from upfront to recurring. Breakeven on a typical conversion is ~18 months, with accretive tailwinds expected from 2027 onwards. Management targets growing informatics from ~$300M to ~$500M by 2030.

On Full-Year Organic Guidance Conservatism

Analyst Catherine Schulte (Baird) asked why 5.5-7% FY guidance followed 7-9% Q1 guidance. Management listed embedded conservatism:

- Academic/government and pharma research assumed not to recover

- China assumed at mid-single-digit growth (vs. 9% in FY 2025)

- No stimulus revenue baked in

- Empower conversion headwinds included

- No reshoring revenue assumed

- Chemistry guided at ~6% (vs. 12% in FY 2025)

On Instrument Momentum

Management emphasized strong momentum entering 2026:

"Orders grew faster than sales in Q4, so we feel very good about where we're starting and the guide we have given for Q1 and the full year. All the drivers are currently fully intact."

LCMS grew high single-digits for every quarter of 2025, with Q1 2026 funnel described as "extremely strong."

Risks and Concerns

- Integration Execution — The BS/Dx business was carved out from Becton Dickinson; standalone operations and synergy realization are uncertain

- China Exposure — While China grew 9% in Q4, the macro environment remains volatile; DRG headwinds pressuring diagnostics

- Leverage — Elevated debt levels post-acquisition (~$4.6-4.7B net debt, 2.4x EBITDA), with interest expense of $179M annually

- Margin Pressure — Adj. EBIT margin guided at 28.1% for FY 2026, reflecting acquisition mix

- BD Baseline Risk — Q1 guidance assumes low single-digit decline in acquired business; execution must improve quickly

Forward Catalysts

Data sourced from Waters Corporation Q4 2025 Earnings Call Transcript and Presentation (February 9, 2026) and S&P Global.